Startup Ground Zero: What I Wish I Had Known Then

- Hubstaff scaled from a $26K investment to $12MM ARR, but low ARPU of $4–$10/user slowed growth — proving that validating your business model early is critical before committing resources.

- Before launch, identify 30–40 specific places your ideal customers gather, test recurring revenue potential, gross margins, and pricing benchmarks to avoid building something the market doesn't want.

- Finding the right cofounder takes deliberate effort — prioritize complementary skills and local proximity for collaboration, and treat critical questions during recruitment as green flags, not red flags.

Hubstaff started with $26K and an idea. The initial goal was to create a business that could do about $15-$20k a month. Now, we’re at $1MM recurring revenue every month — $12MM annual recurring revenue — with more than 85 people on the team.

This isn’t my first startup. Hubstaff is my third “successful” business venture. I’ve also had three failures, and I’ve learned with each experience. Every business is different, so even if you succeeded in a previous venture, that doesn’t guarantee that you’ll be successful again.

But the experience does help.

Hubstaff started with $26K and an idea. Now we do $1MM recurring revenue every month.

People ask me: “If you could start over knowing what you know now, what would you change?”

That’s what I’m going to address in this article. If you don’t have time to read through, bookmark this post because it’s packed with 9 years of experience that I earned the hard way.

Truthfully, if I had it to do over again, I would do things differently.

This was my first software business. Experience is the best teacher, and growing Hubstaff to $1MM MRR has been a steep learning curve.

If you’re at this stage and are looking for direction, here’s what I wish I had known or understood better at ground zero.

Stay in the loop

Subscribe to our blog for the latest remote work insights and productivity tips.

1. Know the goal of your business

When you launch a startup, you’re signing up for some gut-wrenching, white-knuckled work.

If you’re going to get through it, you need to know what you’re doing and why you’re doing it.

Most entrepreneurs are pretty good at knowing what they want to do, but they don’t have a good reason why (AKA “purpose”).

Simon Sinek talks about this in a book called Start With Why. Here’s a TedX talk where he explains why this matters so much.

This was pretty solid for Hubstaff. We knew what we were going to do — after running remote teams, I knew that there was a need for transparency and reliable software. The tools I had tried before either didn’t do what I needed or didn’t function the way they were supposed to.

We had a really solid “why,” too.

People want to be free and live life on their terms. I wanted to own a business where I could do that, my team can do that, and all of our customers can do that. I had experienced this in previous businesses — people always asked me how in the world I worked from my home and made a good living, especially on the internet.

I knew the value of remote work, and we wanted to provide the needed software to other business owners so they could experience the same.

So they could set their businesses up to succeed.

People want to be free and live on their own terms. I wanted a business where I, my team, and all of our customers could do that.

When you run an office, you have to commute and spend hours of your day just sitting in a car or on public transit. You have to waste time managing your office instead of running your business or spending time with family.

People have to build their day around work, so there’s less time for the things that really matter to you, like being around when your kids are small. You can really feel that pain when you read this post from 2015 when I talked about starting Hubstaff.

I feel like this mission gets a little lost sometimes as the company grows, but it’s still there and still important.

If you’re starting at ground zero, make sure you have this part down. It will get you through a lot of tough times and it will help your company remain rooted in what matters. It will provide the vision for people on the team so they make better decisions. It’s kind of like your guiding light.

2. Identify your customers and your market

What’s your ideal customer profile?

Know exactly who these people are: their demographics, the industry they’re in, secondary markets, everything. You need to find out:

- What other tools do they use?

- Why do they want what you’ve got to offer?

Once you know your ICP (ideal customer profile), do your homework and find out how big that market is.

Next, make a list of where you’re going to find these people. There should be 30 to 40 places, both online and offline, where you can connect with your ideal customer. Maybe there are trade shows or magazines, social media groups, whatever.

How are you going to get in front of them?

This step is about more than marketing. Find your customers and talk to them so that you can build a product that they actually want.

Do you know the number one reason that startups fail? By far, the most common reason that startups don’t make it is a lack of product-market fit.

They build things that nobody wants or needs. Imagine a chicken trying to sell eggs to a barnyard full of other chickens — they wouldn’t be in business for very long.

At this customer research step, you’ll see when there might be an issue and quit early enough that you don’t bankrupt yourself.

When you know that you can easily reach your target customer, you can build with a lot more confidence.

The most common reason startups fail is because they build something that nobody wants or needs.

3. Create your model

Those first two steps lay the groundwork to validate your idea. Creating your business model is where you start to see how the pieces fit together and determine if your startup has a chance.

A good model isn’t a guarantee of success, but it will help you spot some of the problems that will probably lead to failure.

Make a list of other products and companies that are solving the problem you want to solve. If nobody is solving this problem, that’s a warning sign. If nobody else serves that market, it might be an opportunity that nobody else has recognized yet, but probably not. The more likely scenario is that there’s not enough market demand to support a business.

Assuming that there are other companies, figure out what kind of business models they’re using. Find the answers to these questions:

- What are their products, and what features do they include?

- What is their pricing?

- Are they volume-based and self-service, or are they low-volume and high-touch?

This information tells you if you need to be heavily marketing-focused or heavily sales-focused from day one. Do you need a lot of customers to make small purchases, or do you need a few big customers that expect white-glove service?

Decide if the most common model is the one you want. You can try something that you don’t already see succeeding in the market, but there’s a higher risk.

4. Build a model profit and loss statement

Now that you’ve done some homework, it’s time to do the math.

List all of the expenses you expect to have when you first go into business. You can hire team members or freelancers if you need to, but don’t go overboard. Only plan on spending for what you really need. You don’t want to overextend yourself before you have revenue coming in.

If you don’t know how to build a profit and loss statement, here’s a free template.

Look back at your model. If you need more focus on marketing, include your ad spend in this budget. For models that rely more heavily on sales, do you need a professional sales team?

Get as detailed as you can and figure out how many units you need to move to cover your expenses. Be sure that you can realistically find that many customers and calculate how long it will take.

Your profit and loss won’t be exactly correct, but it will show you the places where you haven’t put enough thought into your business idea yet.

If I could start Hubstaff over, I would have paid more attention to the size of the market compared to the amount of competition when we created our profit and loss model.

Our growth rate was slower than we anticipated because our average revenue per user was low and there weren’t a lot of people looking for the extra features we offered. It took us a long time to grow our recurring revenue and reach profitability.

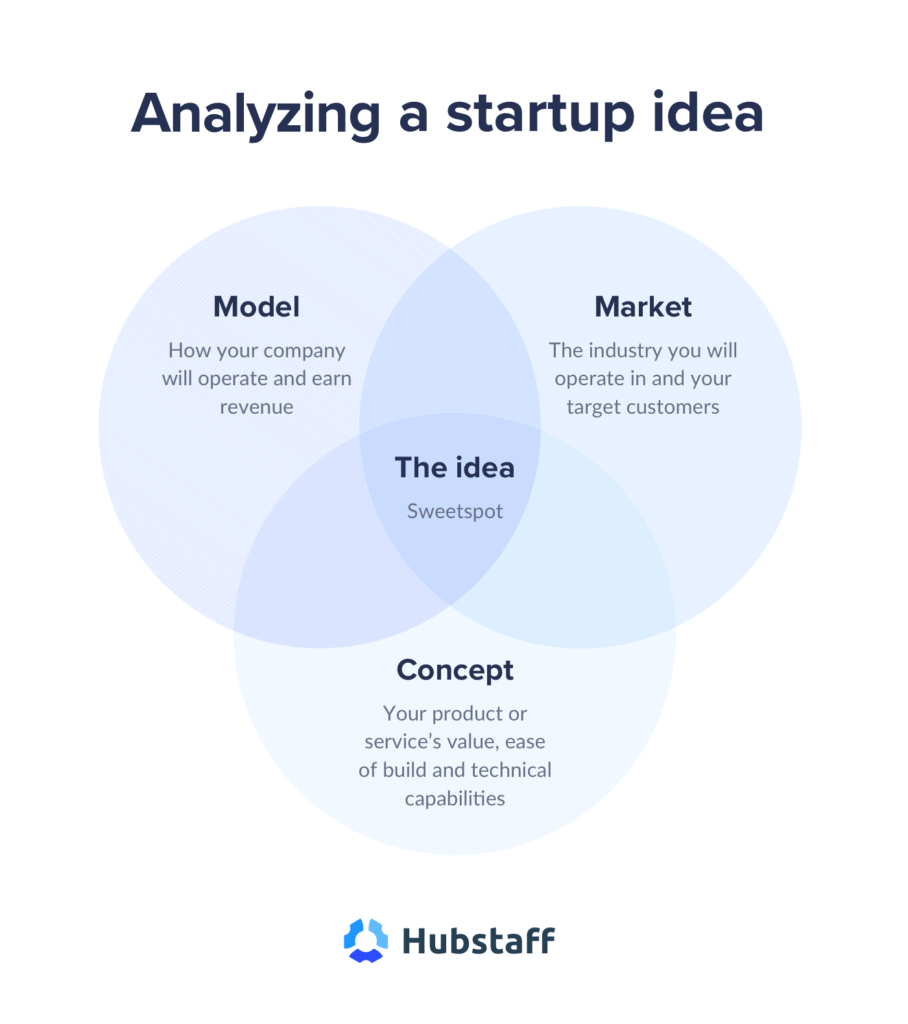

5. Test your startup idea with this model

I’ve talked about the importance of testing your startup idea before. When you get ready to launch a new business, you need to test your idea before you start. This is the pre-flight check on your airplane, and you should never fly without it.

At ground zero, test your model, your market, and your concept. At a high level, here’s how to run your tests.

Model

When I talk about your model, I mean the way your business operates and earns money. A subscription service operates differently than an online retail store, for instance.

We already talked about how to start developing your model in step four. Now, look at your model and see if it meets these criteria:

- You’re set up for recurring revenue

- You have a high gross margin

- The average price your competition charges is high

- You have the opportunity to attract large clients

A good model meets all of these criteria. It’s probably okay if you’re missing one thing, but aim for at least three out of four and understand that you’ll have a much harder time surviving if you don’t check all four boxes.

Hubstaff meets three out of four. In our industry, people usually pay an average of $4 to $10 per user per month, and that makes it harder to scale. This is one of the things I would change if I started over — I would have done more research in this area and approached this problem differently from the start.

Market

Your market is the people who want to buy your product. Drill down and get specific.

Entrepreneurs tend to overestimate how popular their products will be, so be realistic about the people who are actually part of your market.

Take the information you put together in step two and test it with these criteria:

- There’s a large market

- Your customers are easy to find

- You can operate internationally

- You know a lot about this industry and these people

Again, when we started, Hubstaff met three out of four.

- I knew that our customers would be difficult to find starting out, but I also expected the market to grow over time as remote work became more popular.

- We do operate internationally. Our team and our customers are part of global businesses, which helps us know what they need.

- We work hard to understand our customers’ needs and base our new features off of their feedback.

Concept

The concept of your business is the overall idea. It drives what you do every day for the foreseeable future.

Think about the product or service you intend to sell. Does it meet these criteria?

- If you’re building software, it can operate on the web without an app

- You can clearly see the value for your customers

- There’s viral potential

- Adoption or onboarding is simple

- Your brand is recognizable to users

- Support needs are low

- Customers will use your product daily

- It’s easy to build

Your concept doesn’t have to check every box, but use these to help you spot things that will be more difficult than you expect.

These criteria also give you an early warning that your costs may be higher than you want to invest upfront. For example, if you know that onboarding will be complex and your customers need great support, expect to hire good support team agents right away. Build that into your profit and loss model.

Use these points to make your startup idea stronger.

- Can you offer more value and charge more for it?

- How can you generate more recurring revenue?

- Can you make your brand more recognizable as users interact with your product?

If you spot problems in all three areas, go back to the drawing board. Maybe this idea isn’t as solid as you think.

Subscribe to the Hubstaff blog for more tips

6. Find a great partner and sell them on your idea

Running a successful startup is too hard to do by yourself. You need a great cofounder that has the right knowledge and temperament to complement your weaknesses and get things done.

A good cofounder is as motivated as you are. You need to be able to rely on them.

When you split duties, you should fully trust them to do what they need to do without requiring you to call the shots. Each of you should communicate well, but handle things independently. They’re not an employee — they’re a partner.

Most likely, this person will not be your friend who likes technology or builds websites on the side. You’ll have to go out looking for the right person who has the same goals, work ethic, and business priorities as you. I found my cofounder on LinkedIn.

Even if you plan to build your company entirely remotely, I recommend finding a partner locally. You’re both going to put in long hours and solve difficult problems together, so it’s better if you can get in some face-to-face time with them. That familiarity will go a long way.

The thing is, your ideal cofounder is probably already doing something. They’re smart, busy, and selective. That means you will need to sell them on your idea.

When I found Jared, he took almost two weeks to get back to me and told me that he was only entertaining contract opportunities.

Smart people, especially developers, need to hear your pitch. They’ll be critical. They’ll ask questions. All of that is good. Jared said things like, “I’d like my wife to get a chance to meet you,” and “I want to make sure my head and gut are all green flags before proceeding.”

Those statements told me that he’s a critical thinker who makes decisions mindfully, which is exactly what I wanted in a cofounder.

Having built multiple startups, I always recommend having a cofounder on board with you. Do your homework first, then find someone else while you’re still at ground zero.

This was a process and decision I wouldn’t change one bit. The partnership between me and Jared is solid and it’s one of the keys to our success.

7. Create your plan to go to market

From this point on, keep your profit and loss model handy. Treat it like a living document and update it at every step.

If you don’t, your costs can quickly creep up, and you’ll launch a business that doesn’t have a good chance at profitability.

It’s time to get tactical. Lay out your plan to attract your first customers. Where are you going to find them, and how much will it cost you? Decide if you’re going to run ads, attend trade shows, start content marketing, and whatever else you plan to do for marketing at launch.

Build that plan into your profit and loss.

Here are a few ideas to include in your go-to-market plan:

- Draft a messaging matrix, where you define your key messages and communicate your value to different audience segments

- Create a budget for paid ads and determine the best placements

- Map out the customer journey from initial contact to sale and then retention

- Determine if you need a website (yes) and social properties (most likely yes, as well) and budget for that

After this, you’re ready to launch.

8. Structure your team

You’ve got a pretty good idea of what work needs to be done, so now it’s time to determine who’s going to do it.

In the beginning, expect that you and your cofounder will probably do most of the work on your own. Create documentation to make it clear who is responsible for what so that you can divide and conquer rather than working on top of each other.

Prioritize carefully. What are the most important gaps you need to fill, and how will you get that work done? Can you work with a freelancer part-time? Do you or your business partner have any glaring skill gaps that you need to fill with a full-time person?

Remember that managing people takes money and time, so only hire when you have to. Determine how many people you need from day one and what milestones you expect to hit before you grow the team more. You’ll likely be short-handed for a while.

When you’re ready, hire remotely. That way, you have access to the best talent without limiting yourself to your geographical area. You can hire people in different time zones to cover the business when you’re asleep.

9. Build the right foundation for your product

You have to get your product right from the beginning. It’s expensive and time-consuming to try to go back and fix things later. Even if you’re building an MVP, make sure it’s a foundation for the thing you eventually want to build so that you’re not starting over from there.

For software, work with whoever on your team has the technical expertise to pick a tech stack and figure out how you’re going to build. Decide on hosting and clarify who’s responsible for technical decisions.

For other business models, get your supply chain down and determine how you’re going to manage inventory. Do you need to find a warehouse? What about manufacturing?

The point is that you need to spec everything out in detail. You need to know how you’re going to make your product available to your customers.

Building a project spec is a bigger task than you think. There’s so much to figure out. You need to plan the product you’re going to launch and your growth plan on top of that. Your foundation should cover everything you need now and take into account the things you’re going to need to achieve your long-term plan.

10. Question yourself

You should be all-in and totally confident before you pull the trigger. That’s why I recommend that every entrepreneur take a step back, look at the big picture, and honestly question themself.

Are you ready to invest in this? Do you believe in this idea enough to do it for the next 10 years?

Look at all the information, documentation, and models you put together. That should either give you confidence or proof that you’re not ready.

If you don’t feel totally confident and ready to commit after everything you’ve done so far, then go back to the drawing board. You’re not ready to start this business. That’s a good thing because if you’re losing confidence now, your business plan wasn’t viable, and you probably would have realized this after investing all your time and money.

On the other hand, if you’ve been gaining confidence every step of the way, get the rest of the way there. What else is holding you back? This is your chance to address any lingering issues so that you’re ready to jump in with both feet.

11. Get your personal life in order

Startup life isn’t glamorous. Be realistic and make sure you’re ready for this.

What’s your plan for income? Are you ready to live with no income for two years or more? How will you cover your expenses? Some entrepreneurs borrow from their parents, invest their own money, or are supported by someone else. Is this an option for you?

If you have family counting on you, this is much harder. They’re along for the ride, so you should discuss this with your spouse or partner or anyone else who will need to make sacrifices on your behalf.

Consider what you need to do and how long it will take for your business to be profitable.

It’s hard to focus on your startup when your personal life isn’t in order. Are you ready to let some things slide while you build your business?

Things will change a little once you reach profitability, but the first step is to get there. Make sure you’re ready for that.

12. Build your digital presence and brand

At this point, you’re still at ground zero. Even if your product isn’t ready yet, start building your brand and your credibility.

Start a blog and get writing. Promote your content. Write your product copy. Start finding your voice, developing your brand, and building your following. Your go-to-market plan should be your guide.

As soon as you know you’re going to do this, it’s time to start getting in front of your customers and building relationships. Ideally, you want to launch your product with people already waiting to buy it. You can’t afford to wait around and do this later.

Put up your pricing page and product demo pages. Give people a way to get in touch with you or request information so that you can actually talk to your potential customers.

Reach out and talk to them so you really understand what they want and what they’ll buy. Ask if you can call or meet with some of them to discuss what problems they want to solve and find out what they’ve already tried.

At the same time, launch your content marketing efforts and start building your traffic. This takes time and consistent effort. Publish at least one blog post per week that tells your customers how you’re going to help them and how your product is different. Find out what they need help with and walk them through how to do it to better demonstrate your value.

Starting your digital presence now helps you test interest and set yourself up for success when your product is ready to launch.

Plus, you’ll build something that is more likely to do well because you’ve been communicating with actual customers.

Content was a huge focus for us from the very beginning, and it paid off. An ebook on remote team management that I wrote early on is still one of our most downloaded pieces of content. Our blog currently gets over 100,000 unique visits per month, and we’ve built our authority as a leader in remote work and productivity over the years. The landscape has changed drastically, but we’re still heavily focused on our digital presence and have shifted to adapt.

You can get that ebook here.

13. Get backers

You’ve proven your concept, and you have a growing list of potential (or actual) customers. Demos are going well, and you have solid evidence that your startup is poised to grow.

It’s time to get some backers.

I’m not talking about board members. You might be okay with an angel investor, but they should be really good, and you should retain control of your business. You need the freedom to make hard decisions for your long-term success.

Your backers should be people that know you, like you, and trust you. If you recruit people you enjoy working with and who are really invested in helping you, you’re more likely to get the funding you need while maintaining control of your business decisions.

This backing might come from your parents, your doctor, your business mentor, or even crowdfunding. Find people who believe in you and the same things you do. People who can get behind you and your mission will be more likely to invest in your startup.

Getting financial backing at this point lowers your risk. You have more resources to devote to the business, and you don’t have to risk everything you own to do it.

Final thoughts: Go all in

Don’t ask for permission. Don’t wait for someone to validate your idea. Just go. If you need someone else to sign off, you’re not ready to run a startup.

When you see success, that’s a sign that it’s time to go harder. Don’t back off when you finally gain momentum.

Get obsessed. You’re going to think about your business in the shower. You’ll live, eat, breathe, and sleep it, and do whatever you have to do to make it work.

Your first goal is to get to profitability so that you can invest more heavily in this business. Some people think you can back off when you start making a profit, but you’ll kill your business that way.

When you start to see a little success, that’s when you double down and go harder.

If you don’t have this kind of drive, quit earlier rather than later! It’s better to get out before you burn out if you don’t have the obsession to keep this thing going.

Growing a startup means working nights and weekends, reading about it, thinking about it, talking about it, meeting about it, and getting way outside of your comfort zone.

Talk about it with every stranger you meet. Read books that can help you develop new skills and strategies.

Getting to this part is easier when you’ve done everything else on the list. If I started Hubstaff over again, I would have done some things differently, but this is one thing I wouldn’t change. Obsession makes it work.

Most popular

How to Spot and Manage Work Overload Before Your Best People Burn Out

Work overload occurs when the demands placed on an employee or team exceed their available resources, leading to stress, burnout,...

Workplace Productivity Statistics in 2026: What the Numbers Say

For many businesses, having the ability to maximize output without compromising quality gives them a major edge over their competi...

Time Doctor vs. ActivTrak: Which Tool Is Right for Your Team?

Time Doctor and ActivTrak are two of the most powerful and popular time tracking solutions. Both have strong features, and both ca...

Work-Life Balance Statistics in 2026: A Global Perspective

Work-life balance has become a deciding factor in how people, especially Gen Z, choose or leave jobs. The data shows that work-lif...

![How to Identify, Define and Prioritize Business Goals in A Startup [Examples]](https://hubstaff.com/blog/wp-content/uploads/2019/04/Goals-and-Task@2x-780x390.jpg)